(GA 2010)

The main purpose of forecasting business activity and financial results is for planning and decision making purposes. The more accurate the forecasting process, the more accurate the decisions are regarding the operation of the Hotel.

- Objectives of Forecasting:

- Establishing a revenue culture within the organization.

- Being pro-active in adapting to changes in the market’s conditions/needs by making course adjustments to ensure that on-going revenue and profitability goals are achieved.

- Instilling accuracy, timeliness and uniformity of reports to the company’s management and Hotel Owners on the hotel’s financial performance plus establish a discipline within the hotel team.

- Improve scheduling of resources and staffing.

- Ensuring that the hotel has an aligned team focused on performances through the participation of all Division Heads in the monthly, quarterly, and year-end forecasting and financial review. (Team Work)

- Recognize the importance of each Room Market Segment (Room nights, Rates, Revenues) and of the F&B Outlets and Catering revenue potential as well as other sources of minor operating revenues.

- Assist management to identify opportunities in both revenues and expenses, and be proactive.

- Focus on developing strategies and action plans based on agreed objectives.

- Facilitate continuous improvements throughout the hotel.

- Highlight the market position of the hotel and understands the trends in the market.

- Time to identify new targets; what if you invest in sales resources, what if you invest on online marketing, what if you increase your online visibility?

- Forecasts are to be aggressive but achievable.

- Forecast prepared at the hotel will be given to owners/board.

- Responsibilities:

- Every GM’s/Manager is responsible for producing an accurate forecast for following month, for the coming 3 months and for year-end. It is their responsibility to ensure they have a systematic approach of gathering the information and documenting the assumptions. (DOF/FC and DOSM together with the Revenue Manager will assist the GM in compiling the report)

Note:

- YTD positive variance, revenue and profit, should be carried to year-end.

- 12 months rolling forecast to be considered at later date.

- General Manager’s responsibilities – to provide overall guidance and direction to all participants. To explain how important forecasting is and to show how it is used to make business decisions. (Periodic forecasting review at Corporate office presented by GM)

- Credibility – if the 30-day and the 90-day forecast is within +-5% variance, then the year-end forecast carries a lot more credibility and therefore allows for cash flow planning to become more accurate.

- Time – the less time you spend on creating a forecast, the more likely you are to have an inaccurate report.

- Basis (Revenue) :

- Seasonality,

- Previous year,

- Previous month,

- Budget,

- Business on books as compared with past (Booking Pace),

- Movements/travel patterns from geographical sources,

- New supply in the market,

- Loyalty program,

- RSO’s,

- Packages,

- Anticipated events/activities in the market,

- Potential and management of the electronic business; web, OTA’s, mobile, etc.

- Pricing strategies,

- Market share/RGI,

- Others as appropriate.

- Expenses to look at:

- Cost per occupied rooms

- Cost per cover (F&B)

- Labor cost movements

- Cost’s saving plans

- Others as appropriate

- Advantages of Forecasting:

- Use it as a working tool to make business decisions – if Rooms or F&B forecasts a drop in revenue, you have the information needed to respond and act upon it immediately.

- Use forecasting to measure results of your business decisions – i.e. did you generate additional covers by spending the advertising funds? What has been the impact of the rate adjustment? Or the new competitor hotel? What has been the impact of the new sales person? What has been the impact of the new menu pricing? And the impact of closely managing the web-site/portals rates? Increase/decreases from OTA’s and rates? Bookings via web-site, via mobile, by RSO’s, etc.

- Make the best use of everyone’s time – with direction and follow-up, the time and effort everyone spends to develop the information should reflect the best estimates possible based on the information known today. Plugging percentages or cushions into the numbers only distorts the information. All of the assumptions and efforts made to project revenues and expenses are lost by a lump sum “adjustment”.

- Improve awareness and sense of responsibility of Division / Department Heads on their respective department’s revenue, expenses and profitability.

| Authority | This is a GM driven exercise and cannot be delegated. | |

| Co-ordinator | The Financial Controller co-ordinates the forecasting process and prepares the overview/statistics with the assistance of all concerned. | |

| Team Efforts | All Division Heads are involved in the monthly, quarterly and year-end revenue and departmental profitability. Action taken during the P&L review process is RE-ACTIVE and not so much one’s can do. Action taken during the forecasting process are PRO-ACTIVE and you can do something to improve/reverse the situation. | |

| Schedule | Objective is to have the monthly performance review/forecast within the first 7th day of the following month together with the monthly financial report. | |

| Schedule/ Process | Each hotel should develop an appropriate schedule based on their organization/structure. Process should take around 7-8 hours per month (or as needed): – 3-4 hours for revenue. – 2-3 hours for expenses. – 1-2 hour(s) for final report, GM comments, and actions to take to achieve targets. Each of division heads play a role in developing their individual hotels forecast. The more accurate the individual forecast are the better company forecast we have available for our owners. | |

| GM Comments | Prepared and signed by GM, not to be delegated. Clear, concise and informative report. Do not repeat figures. Keep within 1½ pages. Comments to be made on: – Past month, next 3 months and year-end, – Variances in exceed of 5% if not self-evident, – Focus on the “why” not the “what”, and actions. – If year-end GOP shows below budget, highlight major actions being implemented to impact results, first revenue then expenses (easy to cut expenses, hard to improve revenue). |

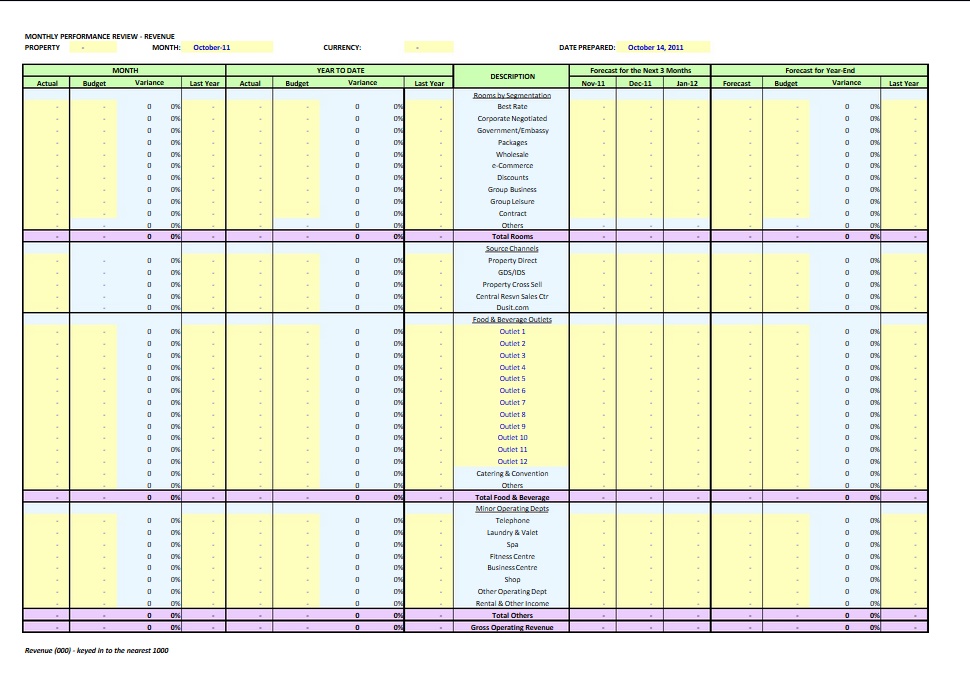

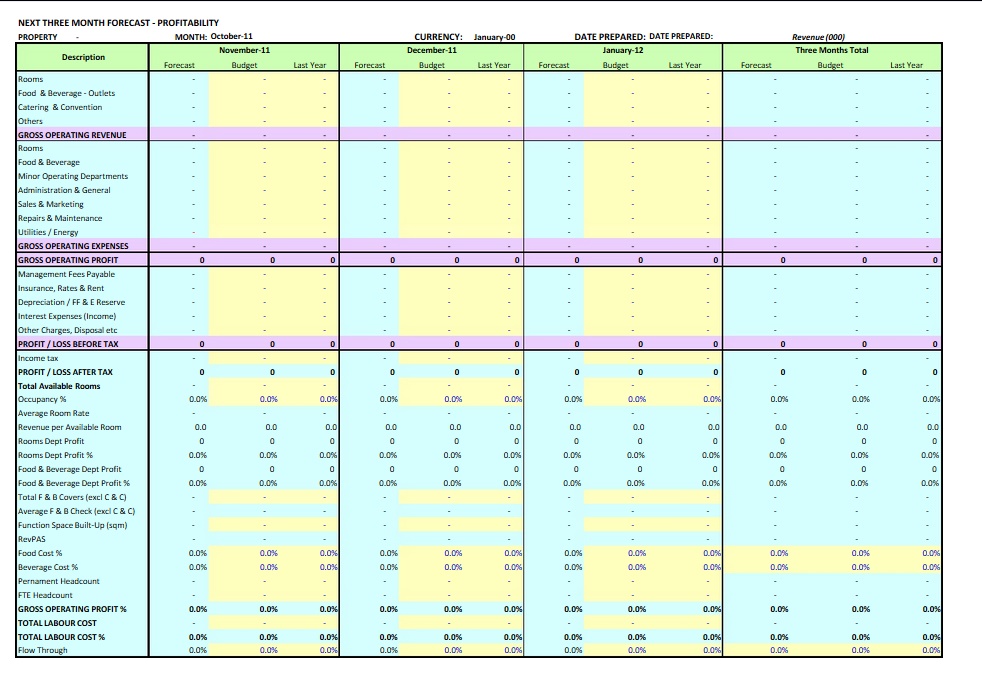

Worksheets to be completed in the Revenue and Profitability Template :

- Cover page:GM Comments on revenue and expenses

- Page 1:Performance summary

- Page 2:Review – Revenue

- Page 3:Comparison of Revenue to Stretched Budget (applicable)

- Page 4:Review – Profitability

- Page 5:Review – Payroll and related benefits

- Page 6:Next 3 months profitability

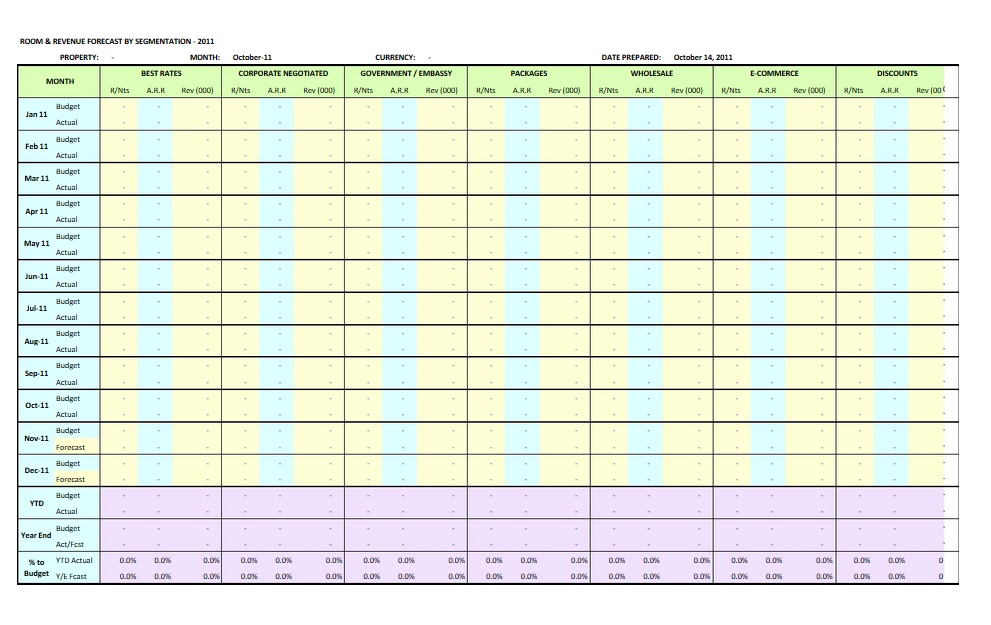

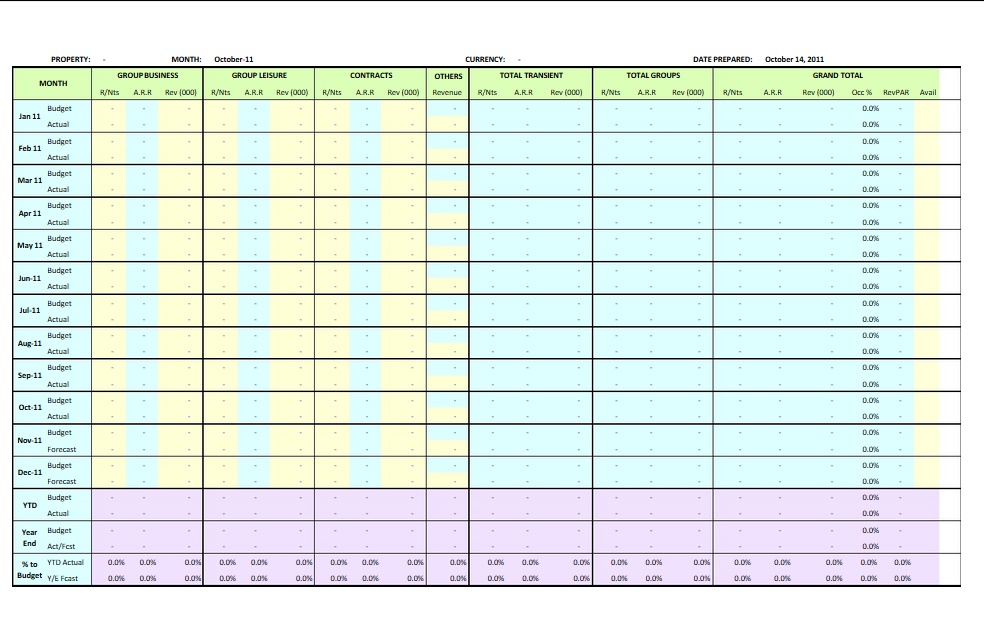

- Page 7:Room segmentation

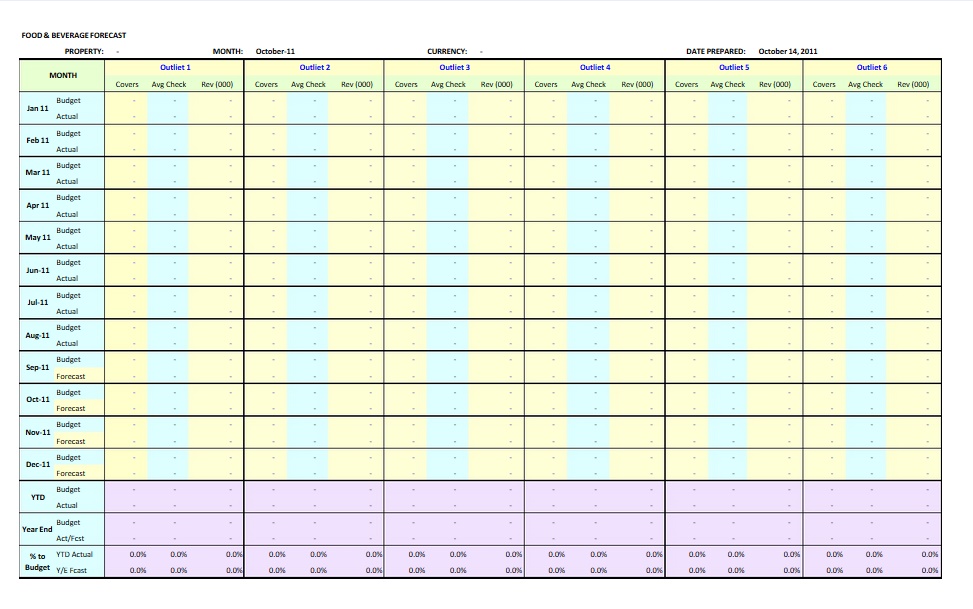

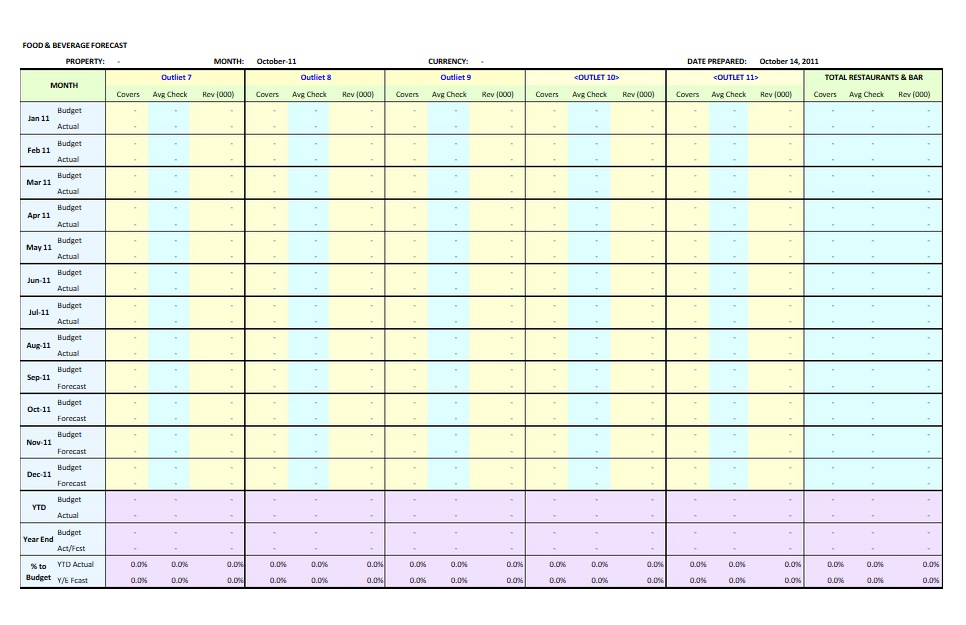

- Page 8:F&B outlets and banquets

- Page 9:Market share analysis

- Page 10:Geographic mix

- Page 11:Top producers

What can you do to improve? (10 Steps)

- Measure performance (forecast vs. actual) closely and understand what went wrong – avoid making the same mistake.

- Provide the tools to the departments preparing the forecast:

a.Provide the standard format assisting the division/department heads to gather the numbers and information (spread sheets for Rooms and for F&B Outlets and Banquets)

b.Identify who needs training.

- Focus on assumptions used to make sure everyone buys into it. Example – Number of walk-ins each day, percentage of group wash, on-months pick-up, major events, new deals with OTA’s etc…

- Focus on revenue calculations – Is there enough documentation on how revenue is calculated? Can you track how the numbers were calculated (#of rooms x rate).

- Prioritize weakness of your forecasting system and work on them one step at a time. For example, rooms revenue always off more than + or -5%? If so, then research why there’s a problem and develop the tools to track the assumptions and prevent it from continuing. Similar approach is recommended for other profit centers and basic expenses.

- Biggest mistake is to spend your time preparing the forecast for other divisions.

Consider developing a “Controller’s Checklist” for forecasting to include such items as:

- Is the math correct?

- Are the details documented, i.e. revenue report calculations.

- How do the numbers compare to the previous numbers?

- Are the changes explained?

- Are the assumptions aggressive but achievable?

- Before the hotel forecast is issued, follow-up and resolve questions.

- Issue forecast to division and explain any areas of concern (red alerts) or any major assumptions that may be different from prior periods.

- Ask yourself “Could you honestly present this forecast to the Owners or to the Board?”

The ideal objective is to have the forecast and the key statistics within a plus or minus 5%. Ensure that you maintain a methodical, systematic forecasting system that accurately projects business results for management decisions.

NOTES:

- Forecasting is representative of GM style and quality of management/leadership.

- Comments should be clear, concise, informative and not repetitive.

- Specify action plans to improve revenue, costs and profitability.

Comments to be written and signed by the GM.

PREPARATION AND FORECASTING CONTROL GUIDELINE

Preparation of the forecast should begin around the 23rd day of the current month as per the recommended schedule mentioned above.

During the month, the GM and the EXCOM team should monitor the Daily Revenue Report and update the forecast for actual results in their respective departmental worksheets. This will help to more closely predict current month results as well as detect trends to use in predicting future months’ results. Again, communication between departments is vital.

A monthly forecast meeting including all members of the EXCOM and Revenue Manager should be held based on the recommended time spent. The result of this meeting should be a day-by-day room revenue and banquet revenue forecast for the next month and an overall forecast for the subsequent two months. The forecast must also be reviewed during the regular Revenue Meetings to ensure that the management team is fully aware of any potential changes that have to be made to ensure that the goals set are achieved.

The forecast should target wage expense as a percent of revenue, with a game plan to meet or exceed budget. To accomplish this,

• Rooms and Catering should have preliminary day by day forecasts of activity

• The EXCOM should review lessons learned from trend history.

• Areas of potential adjustment should be identified.

Upon completion of the forecast meeting, each Division should input their individual department revenue, labor and expense forecasts by day and return to the DOF/FC the consolidated page. The DOF/FC should consolidate individual departmental forecasts into the overall P&L forecast worksheet. Budget and last year figures should be input into this format as well (straight-lined for day by day).

The GM and the EXCOM team should review actual results versus forecast and budget. Variances should be identified at this time and discussed. If necessary, action plans should be developed.

The above process should be completed before the month-end. Once the closing is done, the DOF/FC must then input the actual data for the month into the relevant column.